- 518-692-1200

- 518-692-1222

Getting to Contract

Congratulations! You’ve reached a major milestone: the exciting (and maybe a touch overwhelming) world of buying your first home. The journey of buying your first home is packed with questions, decisions, and, of course, the thrill of finding your perfect place.

Assuming you are not purchasing your first home for cash, your journey to homeownership typically begins with getting prequalified by a lender. The prequalification gives you a rough estimate of how much house you can afford and begins your relationship with a lender.

Once you know how much you want to spend on your home, the search begins. Most buyers first look for a realtor who will begin showing them properties. In our opinion, it is best to find a local realtor in the area where you plan to buy. We have found that realtors who live or work almost exclusively in the area you plan to purchase can provide the most informative guidance on the market.

While every market is different, most buyers will be shown many potential homes before making an offer. Once you have decided on a home, your realtor can guide you in making a competitive offer. Assuming your offer is accepted, you will then begin the process of closing the purchase.

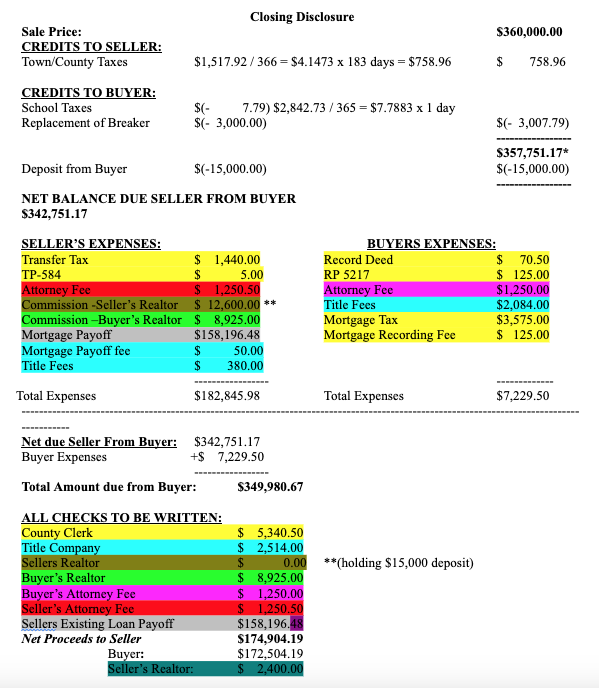

The first step in closing the purchase is entering into a contract of sale. The process of entering a contract of sale varies depending on which New York county you purchase your home in. For instance, in Ulster County, it is customary for the seller’s attorney to draft the contract. However, in Washington County, it is customary for the realtor to draft the contract.

While this might seem like a small difference, it changes the logistics of the sale immensely. For example, if you were to make an offer on a home in Ulster County, you typically must wait to receive the contract from the seller’s attorney while the seller could continue to show the home. Moreover, in Ulster County, inspections are typically completed before entering the contract of sale.

However, in Washington County, the parties usually execute a contract with the realtors, which results in the home no longer being shown to potential buyers. These realtor-drafted contracts should contain an attorney approval provision that allows you to seek attorney approval of the contract within a specified period. In our experience, this results in a less stressful transaction. Also, in Washington County, if you are doing inspections, you would typically conduct them after entering the contract of sale. The contract is then usually written in a way that conditions the contract on the outcome of the inspections.

Because each New York county has different customs, it is best to seek an attorney with experience practicing in the County where you are purchasing your home. Your realtor can be a great resource when looking for an experienced attorney.

Here at Kelly and Sellar Ryan, PLLC, we take pride in guiding new homeowners through the nuances of the purchasing process. We find that our clients appreciate what we believe to be a deep knowledge of the local real estate markets and the individual customs of the various surrounding counties. Anyone with questions about the information contained in this memo can contact Attorney Thomas M. Morelli at (518) 692-1200 or tmm@ksrpllc.com.

Disclaimer: The information you obtain on this website is not, nor is it intended to be legal advice. You should consult an attorney for advice regarding your individual situation. We invite you to contact us and welcome your calls or communications. However, contacting us does not create an attorney-client relationship. Some of the content herein is attorney advertising. Prior results do not guarantee similar outcomes.